Services Week: Will Services now turn into the weakest link of the economy?

We highlighted, analyzed and traded the Manufacturing bottom during the early parts of July during our Business Cycle Week, which proved to be a very well-timed rotational call.

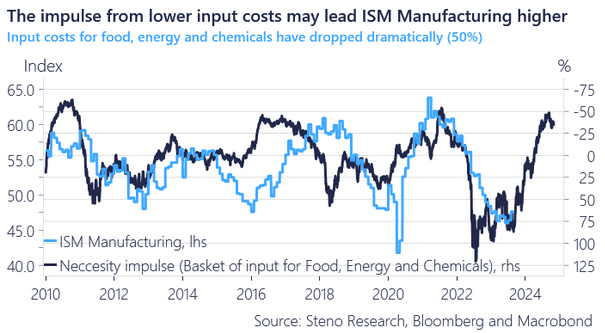

The spread between Manufacturing and Services is highly cyclical and driven largely by relative changes in the cost and input structure of companies.

Our thesis is currently that the shift in input cost structures will start to favour Manufacturing over Services in coming quarters, also as goods prices have started to come down, making them relatively cheaper to services from a consumption standpoint.

Input costs were down almost 50% a month ago in Manufacturing, which compared to selling prices makes it possible to increase margins again in coming quarters.

Chart 1: Manufacturing to see tailwinds from lower costs

When input costs subside for Manufacturers but not for Service companies, the overall economic momentum moves in favour of the Manufacturers. This is most likely the juncture we are at.

0 Comments