Commodity Watch: Alternatives to betting directly on the curve

This week has been all about the yield curve and a potential steepener here at Steno Research. We’ll end the week on a short note for those seeking alternative ways of playing the steepener.

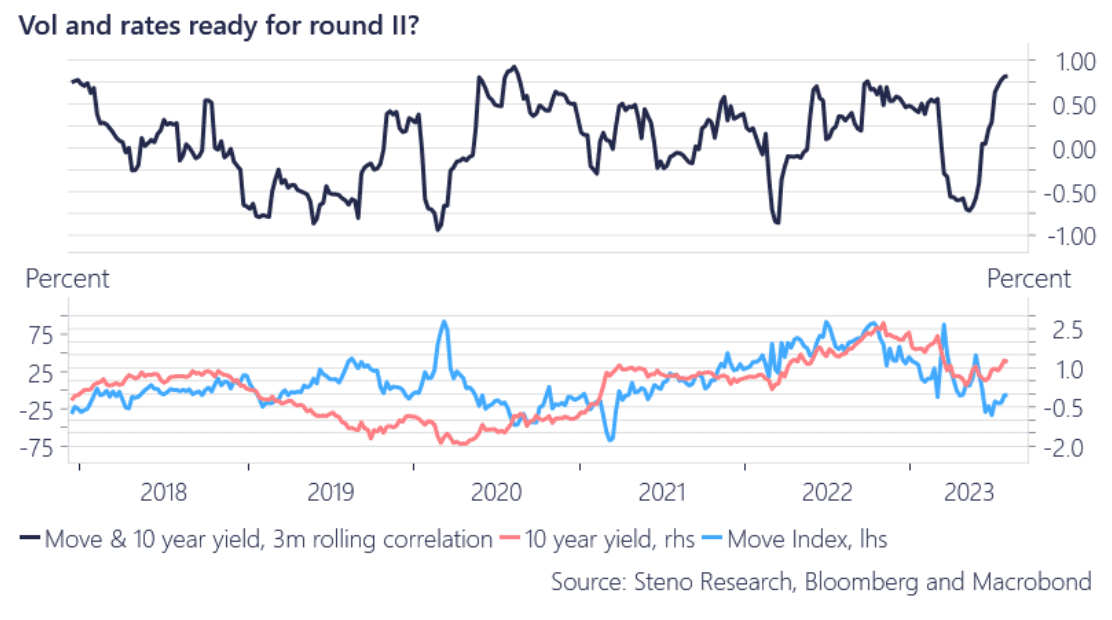

Recently the MOVE and 10 year yield 3m rolling correlation went back to its 2022 levels, so is it time for a cocktail of a rates volatility wrecking ball ala summer 2022 again? Then just short the long end of the curve given the resilient US economy, BoJ’s YCC hikes and a procyclical fiscal policy in the US.

We see this scenario as one in which high duration generation Y & Z assets get hammered and the boomer trade is en vogue.

Chart 1: The Move index and 10 year yield correlation are back to 2022 levels

This week has been all about the yield curve and a potential steepener here at Steno Research. We’ll end the week on a short note for those seeking alternative ways of playing the steepener.

0 Comments