Something for your Espresso: YUUUUGE week ahead!

Morning from Denmark!

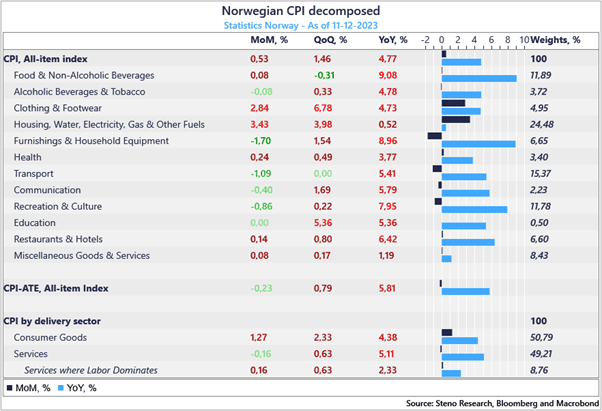

Norwegian inflation printed clearly on the soft side of consensus this morning with clothing and footwear the only “upside surprise”, while transportation costs, recreation and culture and restaurants and hotels all softened up materially in line with our expectations. Core inflation (CPI-ATE) deflates on a MoM basis (not unusual in November).

This once again fits our narrative that European inflation is waning faster than USD inflation and both Swedish and UK inflation is likely going to underpin that narrative over the coming week.

Chart 1: Norwegian inflation softer than expected – detailed composition here

A pamphlet of big central bank meetings is upcoming paired with inflation numbers from several large economies. Will disinflationitas be able to take another victory lap?

0 Comments