Something for your Espresso: May data is way better than April data

Morning from Europe!

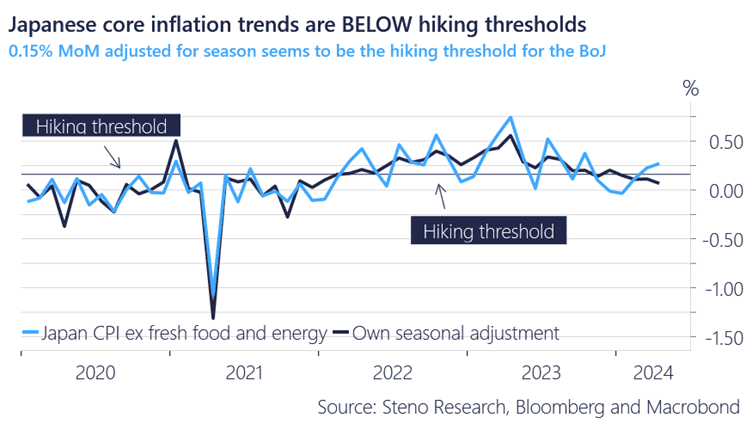

The ex fresh food and energy CPI from Japan printed smack dab at 2.4% in Japan as we expected and it was a soft 0.3% on the month (consensus expected a firm 0.3% reading), so in core terms this was a soft reading AND it was below the 0.15% MoM hiking threshold from the BoJ in seasonally adjusted terms (Our own SA puts it at 7bps on the month)

We don’t think there are imminent inflation risks/hiking risks in Japan, but instead it seems like the JPY yield curve will be allowed to reflate a bit further out as USDJPY settles above fair values here.

Paying 5-10 year JPY rates while not expecting a stronger JPY in FX space seems like a decent structural cocktail here.

Chart 1: No imminent rate hikes in Japan after this CPI report

We are getting confirmation for our “soft patch” thesis in April from data releases right left and center. PMIs are improving and May data will generally look much better than the soft data from April.

0 Comments